This story was originally published by ProPublica.

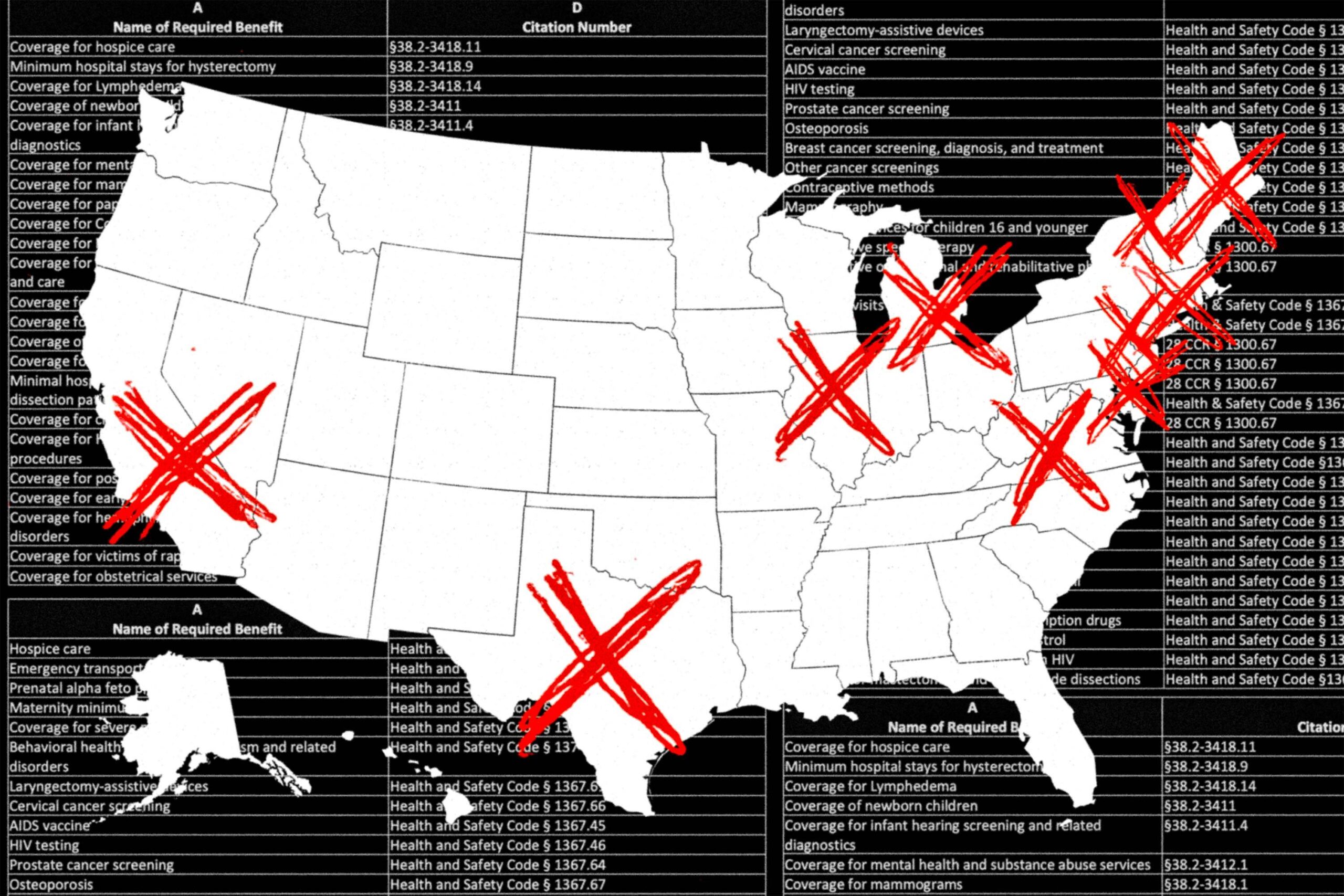

In North Carolina, lawmakers outraged that breast cancer patients were being denied reconstructive surgeries passed a measure forcing health insurers to pay for them. In Arizona, legislators intervened to protect patients with diabetes, requiring health plans to cover their supplies. Elected officials in more than a dozen states, from Oklahoma to California, wrote laws demanding that insurance companies pay for emergency services.

Over the last four decades, states have enacted hundreds of laws dictating precisely what insurers must cover so that consumers aren’t driven into debt or forced to go without medicines or procedures. But health plans have violated these mandates at least dozens of times in the last five years, ProPublica found.

In the most egregious cases, patients have been denied coverage for lifesaving care. On Wednesday, a ProPublica investigation traced how a Michigan company would not pay for an FDA-approved cancer medication for a patient, Forrest VanPatten, even though a state law requires insurers to cover cancer drugs. That expensive treatment offered VanPatten his only chance for survival. The father of two died at the age 50, still battling the insurer for access to the therapy. Regulators never intervened.

These laws don’t apply to every type of health plan, but they are supposed to provide protections for tens of millions of people. AHIP, a trade group that used to be known as America’s Health Insurance Plans, said new mandates are costly for consumers and states, “tie insurers’ hands and limit plan innovation” by requiring specific benefits. Nevertheless, its members take steps to make sure they are following these mandates, the trade group said.

State insurance departments are responsible for enforcing these laws, but many are ill-equipped to do so, researchers, consumer advocates and even some regulators say. These agencies oversee all types of insurance, including plans covering cars, homes and people’s health. Yet they employed less people last year than they did a decade ago. Their first priority is making sure plans remain solvent; protecting consumers from unlawful denials often takes a backseat.

“They just honestly don’t have the resources to do the type of auditing that we would need,” said Sara McMenamin, an associate professor of public health at the University of California, San Diego, who has been studying the implementation of state mandates.

Agencies often don’t investigate health insurance denials unless policyholders or their families complain. But denials can arrive at the worst moments of people’s lives, when they have little energy to wrangle with bureaucracy. People with plans purchased on HealthCare.gov appealed less than 1% of the time, one study found.

ProPublica surveyed every state’s insurance agency and identified just 45 enforcement actions since 2018 involving denials that have violated coverage mandates. Regulators sometimes treat consumer complaints as one-offs, forcing an insurer to pay for that individual’s treatment without addressing whether a broader group has faced similar wrongful denials.

When regulators have decided to dig deeper, they’ve found that a single complaint is emblematic of a systemic issue impacting thousands of people.

In 2017, a woman complained to Maine’s insurance regulator, saying her carrier, Aetna, broke state law by incorrectly processing claims and overcharging her for services related to the birth of her child. After being contacted by the state, Aetna acknowledged the mistake and issued a refund.

That winter, the woman gave birth to a second child, and Aetna did it again. She filed another complaint. This time, when the state made Aetna pay up, it also demanded broader data on childbirth claims. Regulators discovered that the insurer had miscalculated claims related to more than 1,000 births over a four-year period. Aetna issued refunds totaling $1.6 million and agreed to pay a $150,000 fine if it failed to follow conditions listed in a consent agreement.

It was a rare victory. The potential fine, though, constituted less than .002% of the $6.63 billion in profit recorded by Aetna’s parent company, CVS Health, that year.

Aetna spokesperson Alex Kepnes said the company resolved the matter in 2019 to the state’s satisfaction. Kepnes declined to answer why the insurer failed to fix the issue after the first complaint.

Patients often don’t know what care they’re entitled to under state mandates. And one survey found that 86% of people with health insurance don’t know which government agency to call for help. Knowing how to navigate the system can make all the difference to patients socked with giant medical bills.

In December 2022, Samantha Slabyk felt a sudden sharp pain in her lower right abdomen. The San Marcos, Texas, resident took herself to an outpatient emergency clinic, but after a CT scan revealed she had appendicitis, doctors sent her in an ambulance to a nearby hospital. “Everyone indicated that this was an emergency situation that needed to be dealt with promptly,” Slabyk said.

Texas has long had a law requiring insurers to cover medical treatment needed by patients in emergencies. Yet that month, her insurer, Ambetter, wrote in a letter that it would not pay the $93,000 bill because the appendectomy took place at an out-of-network facility.

Slabyk was studying to be a physician’s assistant and had been an EMT. Her fiance’s brother-in-law worked in medical billing and gave her advice on how to push back, as did her mom — whose cancer diagnosis meant she often interacted with health insurers. These connections and experiences gave Slabyk an unusual grasp of her rights and how the system works. Still, every time she reached someone at Ambetter, she felt like she was being stonewalled. Slabyk felt lost.

By June, she was so fed up she decided to submit a complaint to the Texas Department of Insurance. Five days later, she received a call from an Ambetter employee apologizing and saying they would process the procedure as an emergency and pay up.

Centene, Ambetter’s parent company, did not respond to emailed questions or a phone call seeking comment. (The state informed Slabyk it closed the complaint.)

“I was around a lot of people who were knowledgeable and giving me very good advice,” Slabyk said. “And so if you’re just like, on your own, not in the health care system whatsoever, I mean, I just, I can totally see giving up.”

California had to pass not one but two laws to compel insurers to pay for infertility treatments. And one lawmaker said insurers are still saying no often enough that he’s considering introducing a third.

After legislators began requiring such coverage in 1990, some health plans took a narrow view. They refused to pay to preserve eggs, sperm or reproductive tissue for patients facing treatments for diseases like cancer that could impair their fertility. Some patients were delaying chemotherapy to try to get pregnant beforehand or going into debt to pay for treatments out-of-pocket. Regulators forced insurers to pay in some cases, but elected officials worried that other patients were being denied this care.

State Sen. Anthony Portantino worked with colleagues to amend the law in 2019, clarifying that these treatments must be covered. Even so, insurers have been putting up roadblocks.

“Some of the insurers are taking a very strict approach that it has to be chemo,” said Portantino, who is a Democrat. For instance, patients who need cancer surgeries that could leave them infertile have faced denials.

Portantino said he plans to work with California’s largest health insurance regulator to clarify that fertility preservation must be covered more broadly. If that does not work, he said he will turn to legislation once again.

Other regulators are trying to bolster enforcement on the front end. Health insurers submit annual filings to the states where they operate, detailing the treatments and services the company will and won’t cover. Regulators check these policies to figure out whether an insurer is complying with state mandates. In Vermont, the insurance department is using federal grant money to work with an outside company to improve these reviews. Through staff training and education, the department hopes to catch insurers not following state laws before Vermont residents face wrongful denials.

Not all health plans have to follow state mandates. About 65% of employees who get insurance through their jobs work for companies that pay directly for health care. Those companies often hire insurers solely to process claims. Known as self-funded plans, they are regulated by the federal government and exempt from state coverage requirements. Employers increasingly are turning to these types of plans, which tend to be cheaper, partly because they don’t have to cover care that states require. (The federal government also imposes coverage mandates, but state laws can be more robust.)

For patients, this can mean fewer protections from denials.

When 57-year-old Sayeh Peterson, a nonsmoker, was diagnosed with stage 4 lung cancer, her doctors ordered genetic testing to identify the cause. Those tests revealed that a rare gene mutation was, in fact, the culprit for Peterson’s disease and gave doctors the information they needed to create a treatment that targeted the mutation. Her state, Arizona, requires insurers to cover such testing, but Peterson’s UnitedHealthcare plan was self-funded by her husband’s employer, so the law didn’t apply. She and her husband were left with more than $12,000 in bills.

In response to questions, UnitedHealth spokesperson Maria Gordon Shydlo wrote that “there is not enough medical evidence to support use of all those tests.”

As Peterson undergoes a treatment plan tailored to the genetic test results, she is continuing to appeal the denials months later. “We’re told that we have this great insurance,” Peterson said. “But then they deny coverage for the testing that determined what my treatment would be. How do you even get your head around this?”